Why AEO Infrastructure Is the Demand Generation Engine Most B2B Leaders Are Missing

I've watched too many B2B organizations treat their scattered entity signals like background noise.

Different company descriptions across directories. Inconsistent executive bios. Reviews living on isolated platforms with no connection back to a canonical brand entity.

The hidden cost shows up when AI platforms can't confidently resolve who you are. When that happens, your authority stops compounding and starts routing pipeline to competitors instead.

The Breaking Point Where Fragmentation Bleeds Real Pipeline

Entity fragmentation becomes a revenue problem at a specific moment: when AI systems can no longer resolve you as a single, trusted entity for high-intent questions.

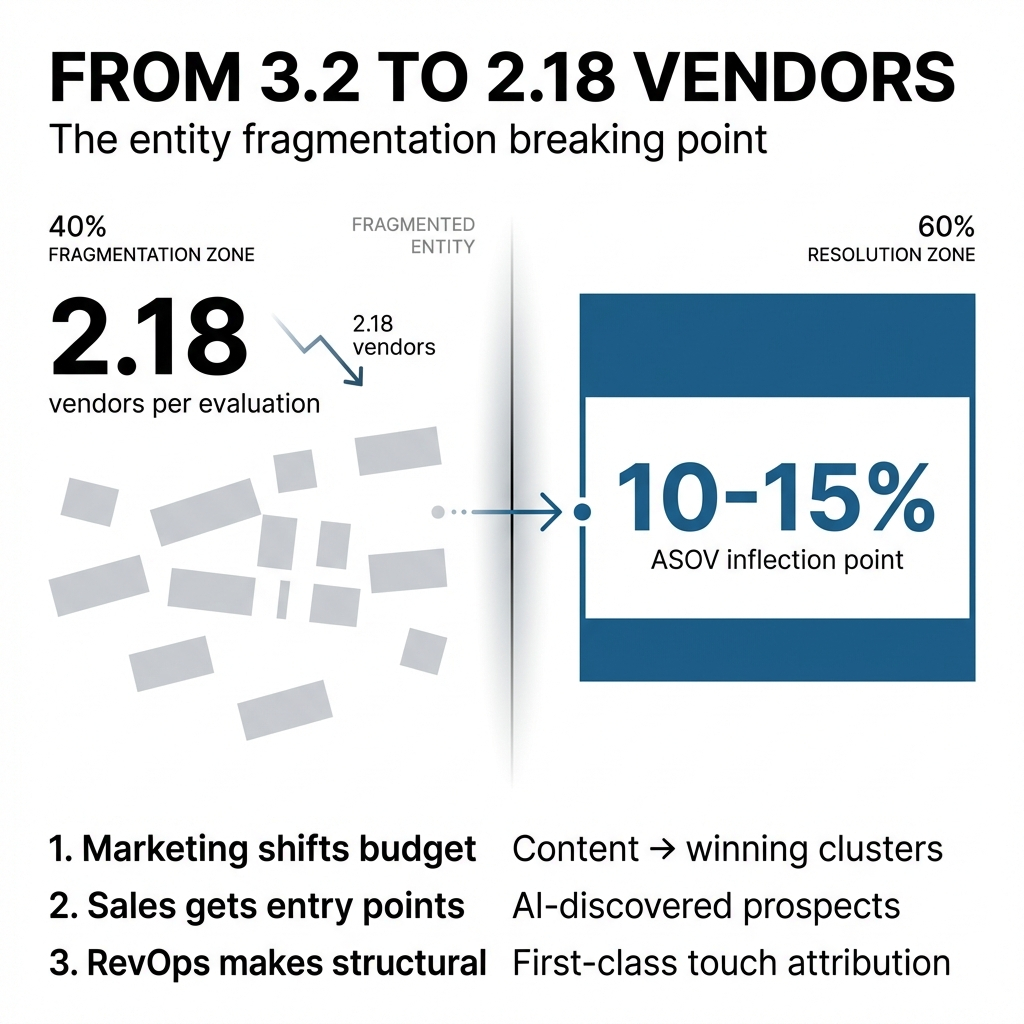

Buyers now interact with 22% fewer vendors compared to last year. Vendor engagements dropped from 3.2 to 2.5, and in the U.S., that figure has shrunk to just 2.18.

The stakes of every buyer contact have intensified. Buyers streamline evaluations to focus only on vendors who passed the research phase with flying colors.

Here's what that looks like operationally:

Entity collision on money queries. When your brand data is inconsistent across sources, AI engines can't confidently distinguish you. They hedge by citing competitors or neutral sources instead. This shows up first on bottom-of-funnel prompts like "best X platform for Y" where engines need a clean, low-risk recommendation.

Confidence scores drop below recommendation threshold. Fragmented profiles and mismatched schema lower AI systems' internal trust scores. You get used as context but not as the cited or recommended vendor. Your content can still be crawled and occasionally quoted, but you stop appearing in shortlists and comparison responses.

Proof lives on separate islands. Reviews, case studies, and PR aren't coherently tied back to a single canonical organization entity. Engines see strong proof but weak linkage, so they attribute it diffusely or to intermediaries instead of you.

The Operational Cost of Being Forced Into Challenger Mode

When AI ecosystems repeatedly surface competitors as the safe defaults, your team gets structurally pushed into challenger mode even in accounts where your product is objectively a fit.

The economics shift dramatically.

As a default shortlist option, buyers are choosing how to work with you. As a challenger, they're deciding whether to rip someone else out for you.

That means more meetings per deal, more senior seller time, and more enablement calories burned per dollar of new ARR. Your CAC goes up, your cycles get longer, and your win rates drop unless you discount or over-invest in sales effort.

You're spending money to manufacture consideration that your rivals are getting for free from answer engines and copilots.

Answer Share of Voice as the Leading Indicator

The first metric I instrument when building AEO infrastructure is Answer Share of Voice for high-intent prompts.

This measures what percentage of AI answers that could create pipeline actually name you as a recommended vendor versus your competitive set.

I define a cluster of high-intent prompts that map to opportunities you care about. Problem queries, solution queries, comparison queries. Then I measure the percentage of AI responses where your brand is explicitly mentioned or listed as an option, divided by all responses where any vendors are named, benchmarked against key competitors.

This gives you a single Answer Share of Voice number for the money layer of AI discovery. It correlates far more tightly with opportunity creation than impressions or raw citations.

Studies show that visitors coming via AI-assisted paths convert several times higher than standard organic because they arrive pre-educated and pre-framed by those answers.

When your Answer Share of Voice rises in high-intent clusters, you typically see parallel lifts in branded search, direct visits, and AI-assisted conversions. That makes it a leading indicator of net-new pipeline creation rather than a vanity visibility metric.

The Operational Shift When You Cross the Threshold

Hitting that 10-15% Answer Share of Voice inflection in a cluster is the moment you stop testing AEO and start re-routing GTM around it.

You treat AI surfaces as a primary demand rail instead of an experiment.

Marketing shifts budget. More dollars move from broad, low-intent awareness into content, PR, and review programs that reinforce the winning clusters and queries where you already have shortlist presence in AI. Content briefs are written around what helps you defend and expand Answer Share of Voice in these clusters.

Sales gets new entry points. SDR and AE teams get explicit sequences and talk tracks for AI-discovered prospects. Reps and regions tied to segments where Answer Share of Voice is strong get more inbound weight and fewer cold accounts because you know those segments now have higher natural surface area with your brand via AI tools.

RevOps makes it structural. AI-assisted becomes a first-class touch type in your CRM and attribution model. As data shows that AI-assisted leads from certain clusters convert faster and at better economics, RevOps can justify shifting headcount, routing rules, and budget toward those journeys.

Over time, your funnel model assumes a baseline contribution from AI surfaces in those clusters, and resourcing is planned accordingly.

The CFO-Level Business Case

The most compelling financial argument is that AEO infrastructure reduces structural CAC for high-intent demand you're already paying for elsewhere, and those gains compound over a multi-year asset life instead of resetting every quarter.

AI-sourced and AI-assisted visitors convert dramatically higher than standard organic or paid. Case studies report anywhere from 10-25x better conversion rates from AI-referred traffic versus baseline organic.

AEO infrastructure that lifts Answer Share of Voice in high-intent journeys has shown 50%+ reductions in cost per acquisition and 250-300%+ ROI within the first 6-12 months. You're capturing demand that would otherwise require expensive ads or outbound to reach.

Unlike paid, those economics keep improving as the Authority Core and entity graph harden. The same fixed infrastructure spend continues to throw off lower-CAC, higher-LTV customers over years, more like an infrastructure asset than a campaign.

In finance language: you're trading a portion of variable, per-click consideration spend for a fixed asset that permanently improves your blended CAC:LTV ratio on the highest-quality demand in your market.

Why This Is Infrastructure, Not Marketing Overhead

Once built, the Authority Core and AI Market Share Analytics layer act like fixed infrastructure. Ongoing maintenance is relatively low, while the incremental cost to capture one more AI-assisted buyer is close to zero compared with paid channels.

Lower structural CAC on a growing slice of pipeline improves EBITDA margins and makes forward revenue more efficient. That's exactly the kind of durable unit-economics story investors reward with better multiples.

The line I draw is simple: You can either keep renting consideration from AI ecosystems at full freight, or you can own the rails that route that consideration to you at a structurally lower unit cost for the next 5-10 years.

For a COO or CFO, that's the moment AEO stops looking like a marketing experiment and starts looking like balance-sheet infrastructure you can't afford not to own.

Comments

Post a Comment